Wall Street loves a safe harbor, and right now, Jim Cramer is pointing everyone toward RTX Corporation (formerly Raytheon Technologies) like it’s a life raft in a storm. The logic is simple, seductive, and fundamentally flawed: global tensions are rising, defense budgets are swelling, and therefore, the biggest players in the "military-industrial complex" are guaranteed wins.

It’s lazy. It’s predictable. It’s exactly how you lose money while the "smart money" exits through the back door.

Buying RTX today isn't a play on global security; it’s a bet on legacy hardware in an era where the rules of engagement—and the economics of defense—just changed forever. If you’re following the lightning round advice to "Buy RTX," you aren't investing in the future of defense. You’re subsidizing a bloated spreadsheet that is struggling to keep pace with a decentralized, high-speed reality.

The Conglomerate Tax You Can't Afford

The biggest lie in defense investing is that bigger is better. RTX is a massive, sprawling entity that tried to marry commercial aerospace (Pratt & Whitney, Collins Aerospace) with pure-play defense (Raytheon). Proponents claim this creates a balanced profile. In reality, it creates a drag coefficient that would ground a fighter jet.

When you buy RTX, you aren't just getting Missiles & Defense. You’re getting the massive liability of the Pratt & Whitney GTF engine crisis. I have watched analysts hand-wave the powder metal defect as a "temporary headwind." It isn’t. It’s a multi-billion dollar systemic failure that has grounded hundreds of aircraft and forced the company to cough up massive compensation packages to airlines.

While the "buy" crowd looks at the backlog of Patriot missiles, they ignore the fact that the commercial side is bleeding cash and management bandwidth to fix a manufacturing screw-up from years ago. You are paying a premium for a conglomerate that is effectively fighting a two-front war against its own balance sheet and its own engineering mistakes.

The Myth of the Infinite Backlog

"Look at the backlog!" is the rallying cry of every bull. RTX boasts a backlog north of $200 billion. On paper, that looks like a decade of guaranteed revenue. In practice, it’s a graveyard of inflation risk.

Defense contracts, especially the massive multi-year ones RTX specializes in, are often fixed-price or have capped escalators. We are living in an era of volatile material costs and a tightened labor market. A backlog signed in 2021 is a liability in 2026. Every hour of labor and every ton of specialized titanium costs more today than when those deals were inked.

I’ve seen programs where the "record backlog" actually resulted in shrinking margins because the company couldn't execute fast enough to outrun the rising cost of components. RTX isn't just a defense company; it’s a massive project management firm that is currently underwater on its most important resource: time.

Drones vs. Dinosaurs

The most dangerous misconception in the current market is that high-end, expensive platforms are the only way to win. The "lightning round" logic assumes that because RTX makes the most sophisticated (and expensive) systems, they own the market.

They don't.

Modern conflict is proving that a $50,000 kamikaze drone can disable a multi-million dollar asset. The era of the "exquisite" platform—the $100 million jet or the $2 billion destroyer—is facing a crisis of relevance. RTX is the king of the exquisite. They build the Ferraris of the battlefield. But the world is currently buying fleets of Toyotas with machine guns bolted to the back.

The Pentagon is already shifting. Programs like "Replicator" are designed to pivot toward mass-produced, low-cost, autonomous systems. RTX’s entire business model is built on high-margin, low-volume, slow-to-produce hardware. They are the IBM of 1985—dominant, proud, and completely oblivious to the fact that the "personal computer" of warfare is about to make their mainframes look like museum pieces.

The Valuation Delusion

People call RTX a "value play." Let’s look at the math.

At current levels, you are paying a forward P/E that rivals high-growth tech companies, but for a company with mid-single-digit organic growth. You are paying for safety that isn't there.

$$P/E = \frac{Price\ Per\ Share}{Earnings\ Per\ Share}$$

If the "Earnings" part of that equation is suppressed by $3 billion in engine recalls and the "Price" is inflated by retail investors following TV pundits, the result is a trap. You are buying at the top of a cycle, fueled by geopolitical fear, while the internal fundamentals are deteriorating.

Compare RTX to the emerging "Defense Tech" sector—companies like Anduril or the more agile mid-tier players. These firms are building software-first, hardware-agnostic systems. They aren't burdened by 100-year-old manufacturing plants or legacy pension obligations. They are the ones who will capture the shift in DOD spending. RTX is just trying to protect the status quo.

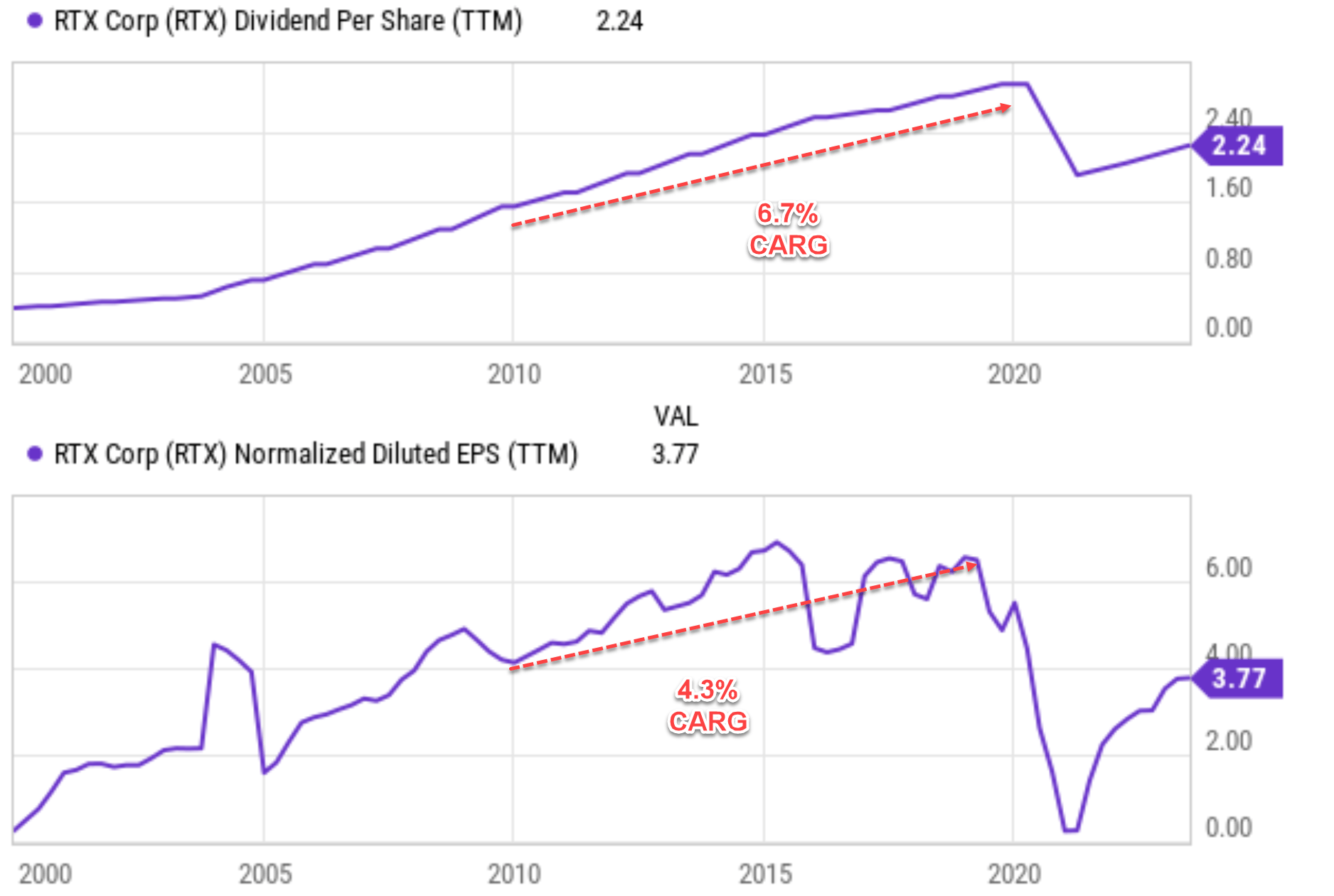

The "Dividend" Distraction

"But the dividend is safe!"

Is it? A dividend is only as safe as the free cash flow supporting it. When a company has to divert billions to fix engine defects and settle with the DOJ over pricing disclosures—as RTX has had to do recently—the dividend becomes a golden handcuff. It prevents the company from reinvesting in the R&D needed to fight off the Silicon Valley upstarts currently eating their lunch in the autonomous space.

If you are buying a stock because a guy on TV yelled about a dividend during a 30-second segment, you aren't investing. You’re gambling on the hope that someone more informed than you doesn't notice the cracks in the foundation.

The Professional Reality

I’ve spent enough time around DC lobbyists and procurement officers to know how this ends. The "Big Six" defense contractors aren't going away, but they are becoming utilities. They will have capped profits, endless oversight, and stagnant growth.

The real money isn't in the companies that build the hulls; it’s in the companies that build the brains. RTX is a hardware company trying to pivot to software in a culture that still prizes "bending metal" above all else. That cultural inertia is a death sentence in the 2020s.

Stop looking for safety in the giants of the past. The "lightning round" is designed for entertainment, not for wealth preservation. RTX is a bloated, legacy-heavy conglomerate disguised as a defensive play.

Dump the dinosaurs before the meteor actually hits.